The final results for 2025 confirm that the guidance has been fully achieved in each aspect, highlighting a significant increase in orders received. A dividend of €1.05 per share has been proposed, in line with the proportional growth in the group’s profits.

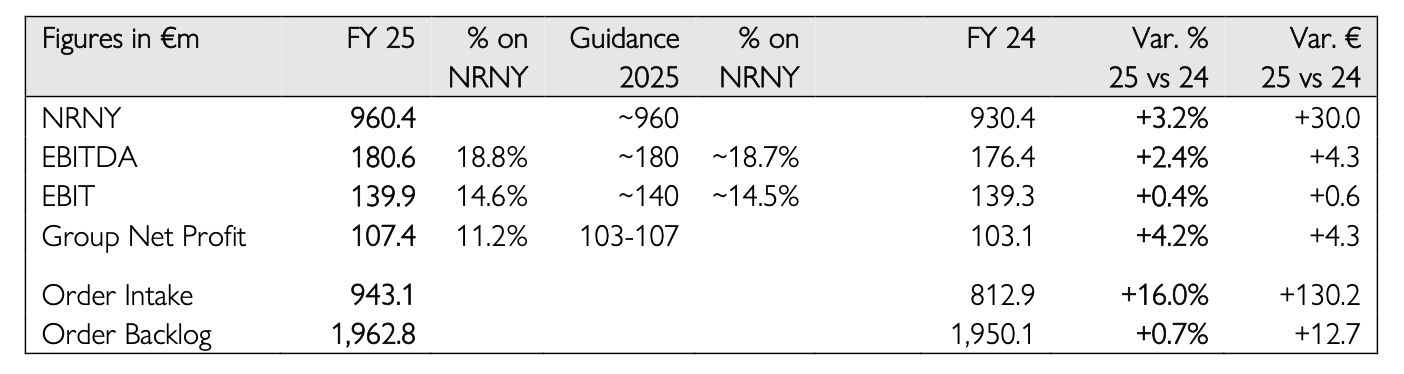

2025 growth across the main metrics sees all financial targets achieved, with Group Net Profit of €107.4 million (+4.2% YoY) and €3.04 EPS net of treasury shares. BoD proposing a €1.05 DPS for FY 2025 (34.6% payout ratio).

Material acceleration in demand across the portfolio: €943.1 million Order Intake in FY 2025 (+16.0% YoY), representing a €130 million uplift compared to the previous year – driven by the success of extraordinary new model launches and enduring brand desirability and strengthened distribution in MED, APAC and U.S.. Q4 2025 marks the 6th consecutive quarter of YoY growth in Order Intake, with €253 million new orders collected in the quarter (+10.1% YoY).

Exceptional order book, with €1.96 billion Order Backlog. 88% of orders are secured by final clients, reflecting the superior quality of the order book and Sanlorenzo’s scarcity model. Net Backlog consistently above €1 billion, thanks to a FY 2025 book-to-bill ratio of ~1x, which maintains the Net Backlog at solid levels over time while growing the top line.

The Board of Directors of Sanlorenzo S.p.A., chaired by Mr. Massimo Perotti, approved the consolidated financial statements and the draft separate financial statements as of 31 December 2025.

Massimo Perotti, Executive Chairman, commented: “In line with the preliminary release, our actual FY2025 results confirm a strong performance, reflecting the enduring appeal of a brand deeply valued by connoisseurs and a vision delivered with consistency. Even in a global environment influenced by several factors of external instability, including the new developments in the Middle East, Sanlorenzo continues to distinguish itself through positioning, innovation and scarcity. We hold a strong Order Backlog, representing more than 1 billion euros on a net basis, made up of high-quality orders which reflect the privileged relationship we nurture with a growing global club of sophisticated yacht owners. The strengthening of our direct distribution network with Simpson Marine across APAC and Sanlorenzo Med in Europe is paying off, increasing our proximity to clients. At the same time, when combined with the scarcity of our volumes, our direct sales footprint – from Florida to Hong Kong, and Cannes to Sydney – allows us to respond quickly to the evolution of demand across different geographic areas. Avoiding any risk of dealer stock build-up typical in the industry at times of changing market dynamics”.

Perotti then continued: “With respect to the Middle East, our direct exposure is limited, at around 7% of revenues. We continue to monitor the geopolitical situation closely, and it is worth noting that many of our Middle Eastern clients use their yachts primarily in the Mediterranean. We keep seeing the region as an attractive long-term growth market.

Massimo Perotti

A highlight of 2025 is Nautor Swan achieving net income profitability in just its first year of consolidation. Operational initiatives remain on track, efficiency actions are progressing, and business development is accelerating, with new product lines expected to strengthen the margin mix in the coming years. We have entered 2026 with a promising start and look forward to presenting our new Business Plan on 8 May at Casa Sanlorenzo in Venice, together with the Q1 2026 results, as we host our first proprietary exhibition during the Biennale Arte”.

FINANCIAL HIGHLIGHTS:

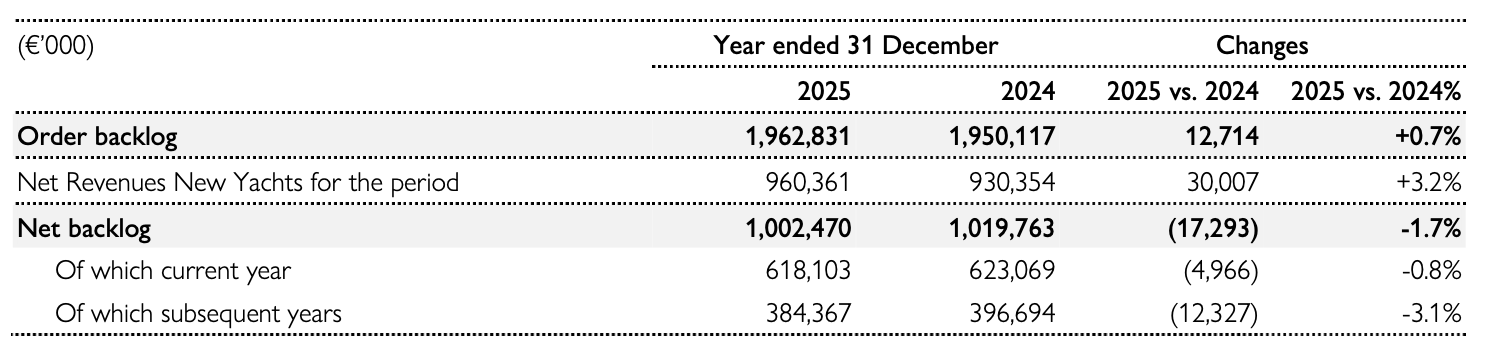

Order Intake at €943.1 million (+16.0% YoY, +€130 million YoY), validating the strength of the brand and the high product differentiation. Even in a challenging context, the Group confirmed its ability to collect significant orders despite scheduled contractual deliveries extending up to 2029. As of 31 December 2025, Sanlorenzo Group is strong of a €1,002.5 million Net Backlog, already in hand thanks to existing acquired orders, of which €618.1 million are related to 2026, benefiting from a significant level of coverage already at the beginning of the year, and €384.4 million related to 2027 and beyond providing a consistent level of visibility into future years.

Order Backlog at €1,962.8 million as of 31 December 2025, +0.7% year-on-year, 88% of which is already sold to final clients, demonstrating its exceptional quality.

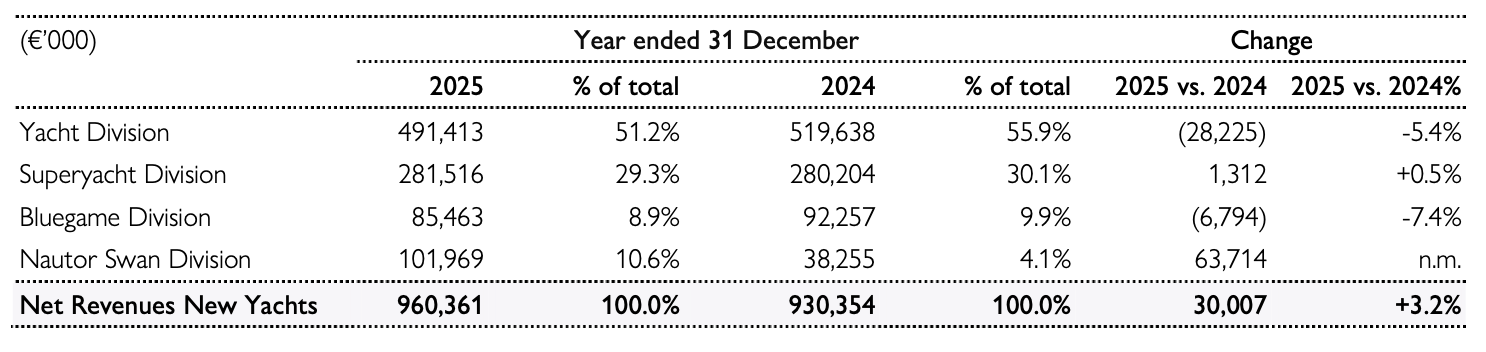

Net revenues from the sale of new yachts (“Net Revenues New Yachts”) at €960.4 million (+3.2% YoY) compared to €930.4 million in 2024. The Yacht Division recorded €491.4 million (-5.4% YoY) with a strong Q4 (+8.2% YoY) with larger units kicking into production after the shift in Q3. The Superyacht Division recorded €281.5 million (+0.5% YoY) while the softer Q4 (-10.0%) was linked to production seasonality after an intense delivery season. The Bluegame Division recorded €85.5 million (-7.4% YoY), successfully navigating headwinds in the segment below 24mt. Finally, Nautor Swan contributed €102.0 million with exceptional performance (+45.1% in Q4 25 vs Q4 24), confirming integration achieved and the rationale of the acquisition.

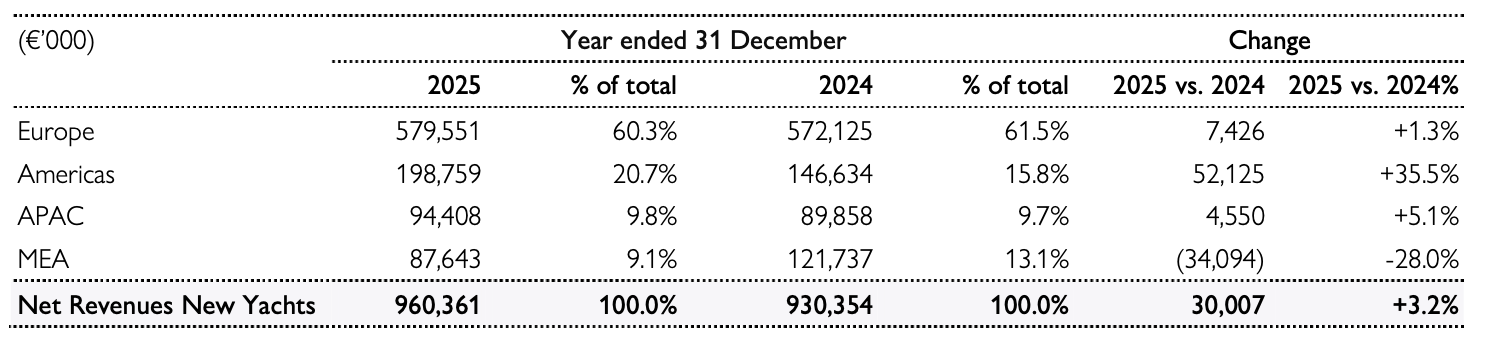

Geographically, strong YoY revenues increase in Americas (+35.5% YoY), whose incidence stands at 20.7%, supported by further penetration in new markets in Central and South America. APAC (+5.1%) performed well, reaching €94.4 million, marking a strong uptick in the Far East and confirming the integration achieved with the Simpson Marine strategic platform. Europe’s (+1.3% YoY) performance was affected by a shift in Q4 to a more balanced quarterly global mix in favour of APAC approaching the yachting season, while MEA (- 28.0%) showed physiological lumpiness given the low-number/high-average-ticket market (+100.0% in Q4 25 YoY). Within the MEA region, Middle East accounts for around 7.7% of FY 2025 NRNY.

EBITDA at €180.6 million (+2.4% YoY), with an 18.8% margin on Net Revenues New Yachts, decreasing by 20 basis points compared to the previous year, confirming the solidity of the Group’s business model and its ability to successfully sell and execute high-value projects. EBITDA margin thus remains broadly stable even after the dilutive effect of the first year of 12-month consolidation of Nautor Swan; without Nautor Swan, margin expansion has been sustained by the accretive product mix, pricing power and a predominantly variable cost structure which ensures profitability resilience.

EBIT at €139.9 million (+0.4% YoY), with a 14.6% margin on Net Revenues New Yachts. The result reflects higher depreciation and amortisation mainly due to the full-year consolidation of Nautor Swan, which includes the effect of legacy investments made prior to the acquisition, as well as the Group’s ongoing investments in product development and production capacity.

Group Net Profit at €107.4 million (+4.2% YoY), with a double-digit (11.2%) bottom-line marginality on Net Revenues New Yachts. Parent company Sanlorenzo S.p.A. Net Profit at €90.4 million; proposed dividend of €1.05 per share for FY 2025.

Organic Net Capex at €48.2 million, with an incidence of 5.0% on Net Revenues New Yachts, a decrease of 0.3% compared to 2024. Around 89% of investments were expansionary, mainly dedicated to the expansion of industrial capacity and direct distribution footprint, as well as to the development of new models and product ranges. Total Net Investments for the period, including perimeter changes referred to the consolidation of Arturo Foresti (strategic supplier of Bluegame operating in the field of electrical systems) and Mediterranean Yacht Management (in-house brokerage company of Nautor Swan), amounted €49.4 million.

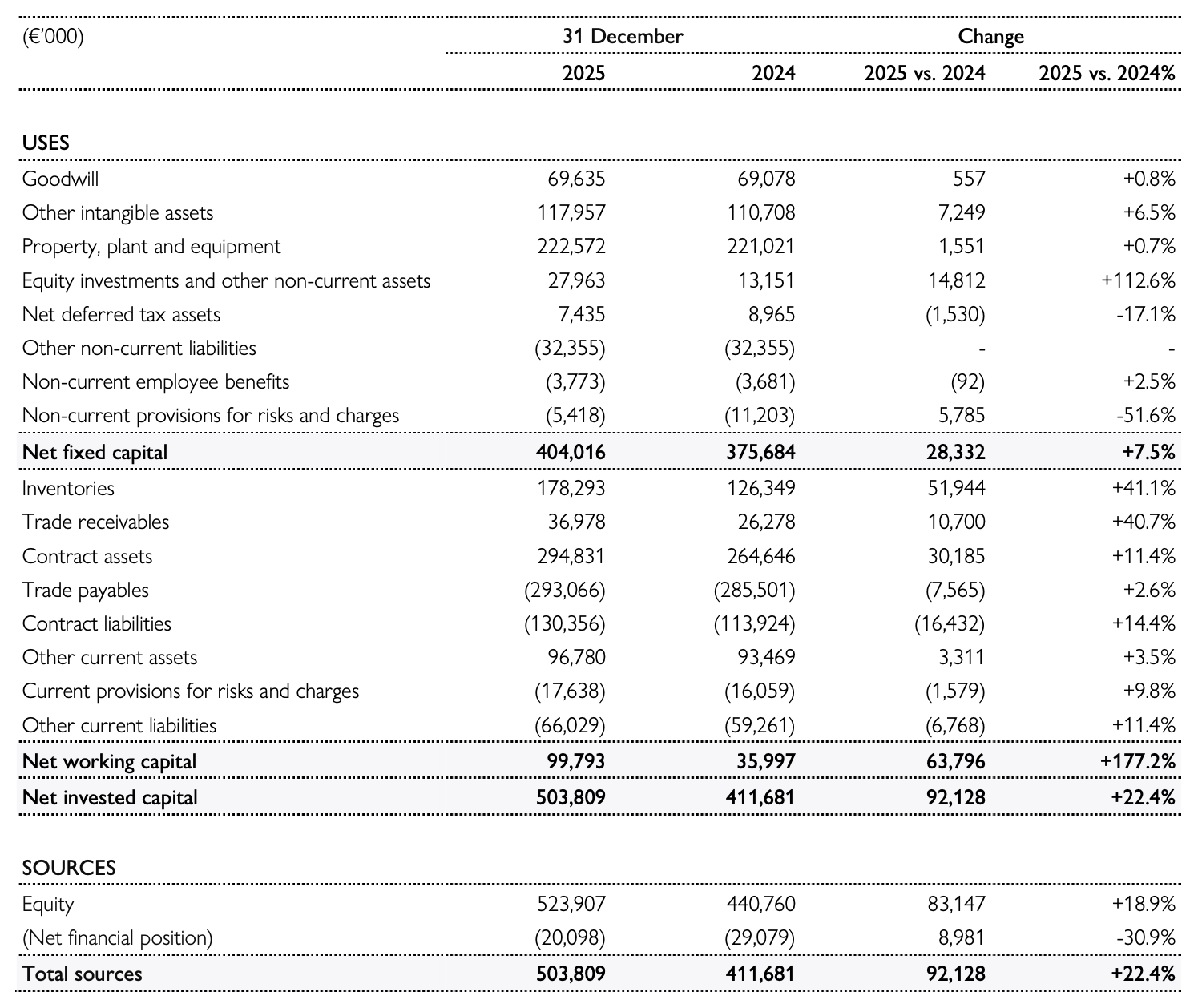

Net Working Capital at €99.8 million as of 31 December 2025 (vs €36.0 million as of 31 December 2024), mainly reflecting the support to the expanded direct distribution network.

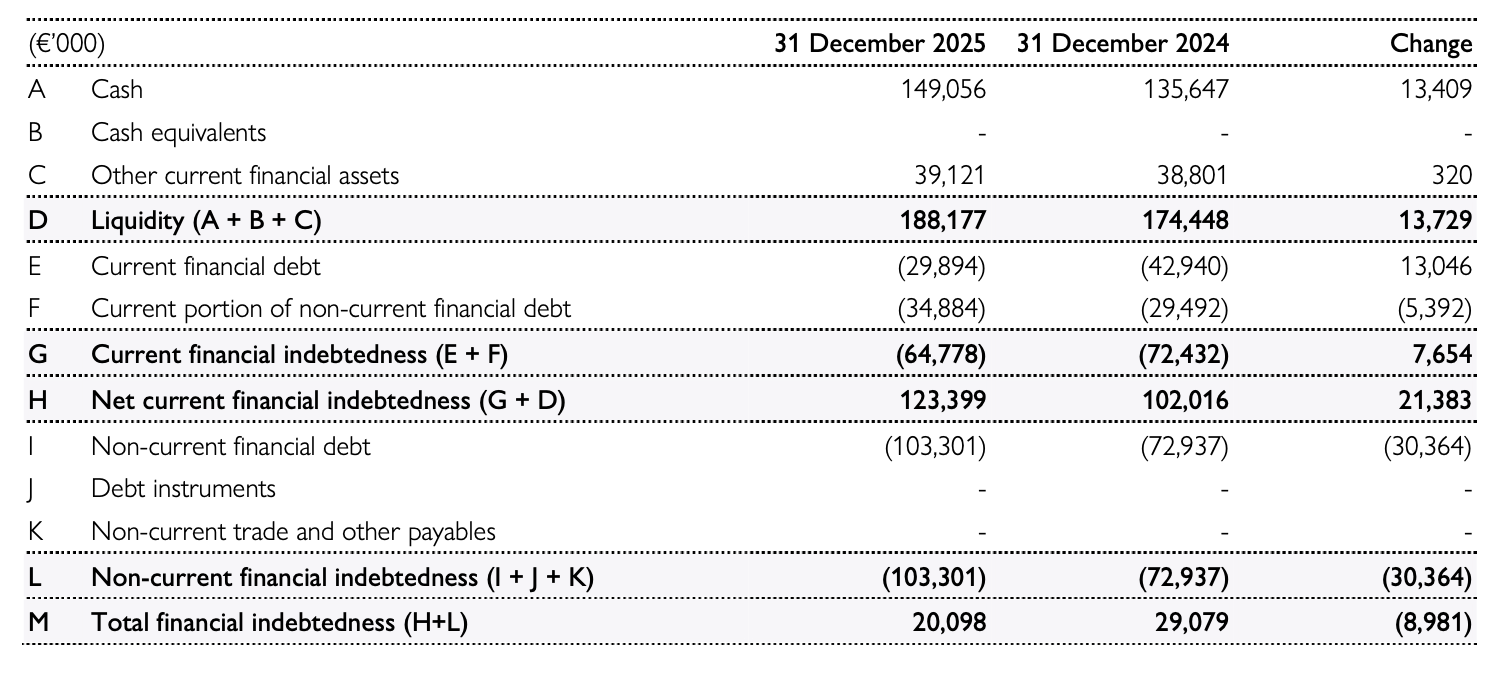

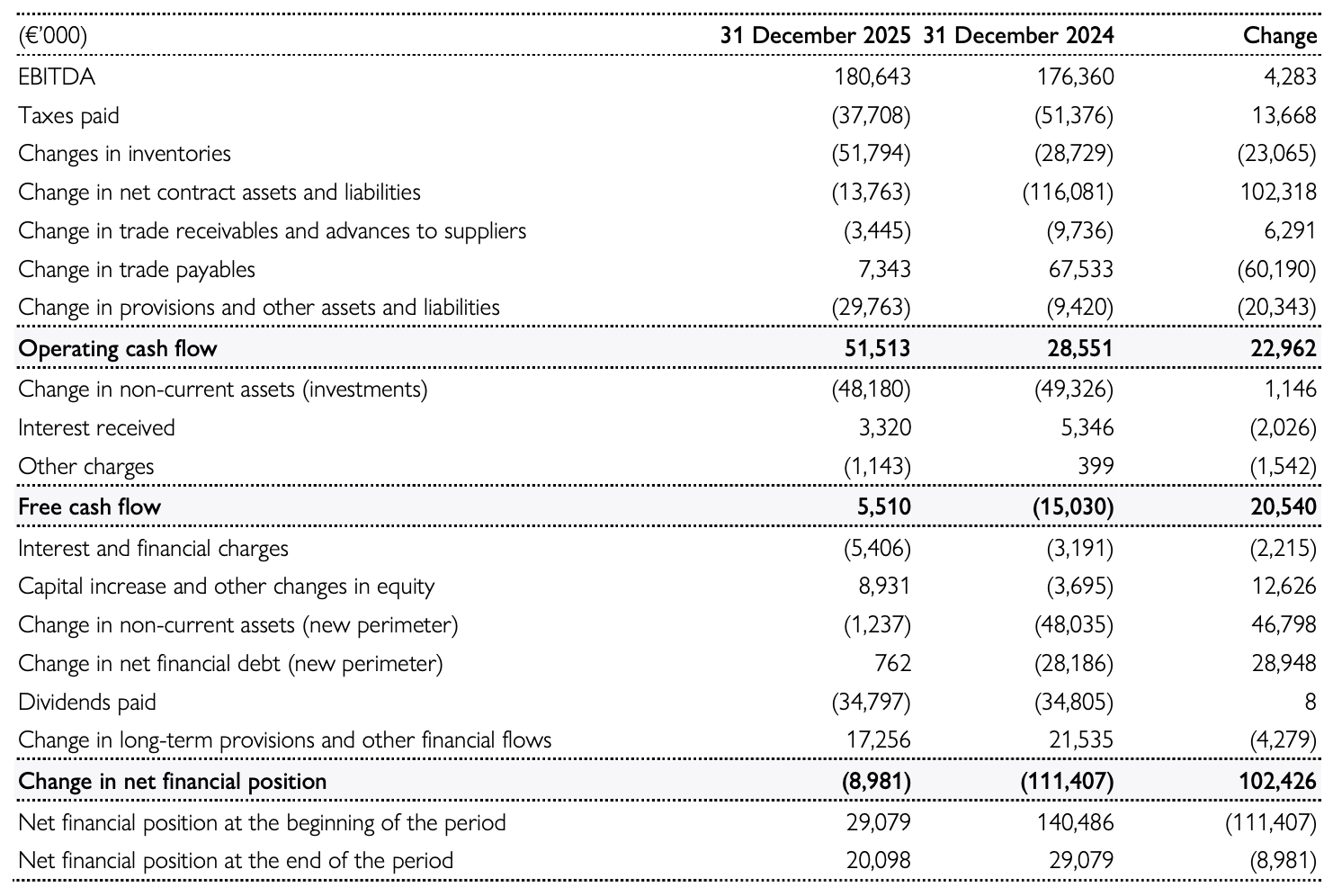

Net Cash position at €20.1 million as of 31 December 2025, compared to a Net Debt position of €14.0 million as of 30 September 2025, implying net cash generation of €34.1 million in Q4 2025. The Net Cash position as of 31 December 2025 includes €28.0 million of IFRS 16 liabilities.

Guidance 2026 to be released together with the Business Plan 2026-2028, to be presented on 8 May 2026 at Casa Sanlorenzo in Venice.

THE BOARD OF DIRECTORS HAS ALSO:

proposed a dividend of €1.05 per share, with a payout of 34.6% of Group Net Profit.

approved the 2025 Consolidated Sustainability Report in compliance with Italian Legislative Decree n. 125 of 6 September 2024, marking the second reporting exercise on environmental, social, and governance matters.

conferred powers on the Chairman and Chief Executive Officer to convene the Ordinary Shareholders’

Meeting on 24 April 2026, on first call, in accordance with the law.

OPERATIONAL HIGHLIGHTS:

Sanlorenzo achieved Top Employer Italy certification in 2025, reaffirming its leadership position in yachting and the Group’s commitment to investing in workplace culture, safety, inclusion, and talent development initiatives.

Sanlorenzo opened its new Americas headquarters and customer lounge at Pier Sixty-Six Marina, Fort Lauderdale, on 30 October. Timed with the Fort Lauderdale International Boat Show, the opening underscores the brand’s expansion across the Americas and its long-term commitment to this growth region.

Sanlorenzo expanded its global distribution footprint by incepting local presence through exclusive leading established brand representatives in high-potential, underpenetrated geographies (Brazil and Mexico) and new geographies (Japan and western Australia).

Sanlorenzo debuted the new 58 Steel in November 2025, presenting a new benchmark in superyacht design between 55 and 60 metres, introducing a revolutionary diesel-electric system reducing emissions by 10% and noise levels to near silence, whilst unlocking new interior volumes. The first Perla Lunar is on the water, with a second hull already in production.

Sanlorenzo unveiled SHE, the new Sanlorenzo Heritage model that fuses timeless design with IPS hybrid-electric propulsion on 22 October. The global reveal led to first client orders confirmed within a week of launch.

On 1 October, the company revealed 74Steel, Sanlorenzo’s newest flagship superyacht, ahead of its launch from La Spezia. The 74Steel is the largest yacht ever crafted by the yard and reinforces Sanlorenzo’s influence in the larger- yacht category while maintaining its focus below 2,000 GT.

Sanlorenzo took centre stage at the major autumn yacht shows in Cannes, Monaco, Genoa, and Fort Lauderdale. In Cannes, the SL110A, SX120, and SD132 made their public debuts, confirming the strength of demand from our customers, proven by the fast conversion into orders already in Q3, with the Yacht Division alone posting more than €200 million of Order Intake, as well as by the significant pipeline of negotiations building up for the coming quarters.

Nautor Swan debuted two new models: the Swan 51 at the Cannes Yachting Festival and the Maxi Swan 128 at the Monaco Yacht Show, alongside the release of the first renders of the Swan Alloy 44. Together, they strengthen the Group’s leadership in the high-performance sailing segment.

Bluegame introduced the new BGF line featuring foil technology developed from its hydrogen-powered America’s Cup tender programme. The BGF45, the range’s first model, premiered at Cannes.

The inaugural exhibition, Breathtaking by Fabrizio Ferri, opened at Casa Sanlorenzo in Venice on 1 September to critical acclaim. First opened during the inaugural Venice Climate Week, the cultural hub of Sanlorenzo Arts celebrates the meeting of art, design, and the sea, strengthening brand storytelling and customer engagement.

The new SX120 and SL110A were launched to acclaim in July, marking significant expansions of the brand’s most emblematic yacht lines and fully aligned with its product strategy in the 30-50 metre segment, reinforcing Sanlorenzo’s leadership in the sweet spot of the market. Joining the SD132, these three latest additions to Sanlorenzo’s acclaimed Asymmetric, Crossover and Semi-Displacement lines were premiered to clients and the yachting community at the Cannes Yachting Festival.

Firmly committed to Road to the 2030 sustainability roadmap with tangible progress, including the development alongside MAN of technology for the trailblazing 50 X-Space, the first yacht with bi-fuel green methanol propulsion, capable of reducing emissions during navigation by up to 70%, setting a new standard for sustainability in the yachting sector, with the yacht now targeted for launch before the end of the decade.

Global and regional leadership was strengthened in 2025 with the appointment of Renato Bisignani as the Group’s first Chief Marketing & Communications Officer and Daniele Lucà as Chief Executive Officer of Sanlorenzo APAC.

CONSOLIDATED NET REVENUES NEW YACHTS

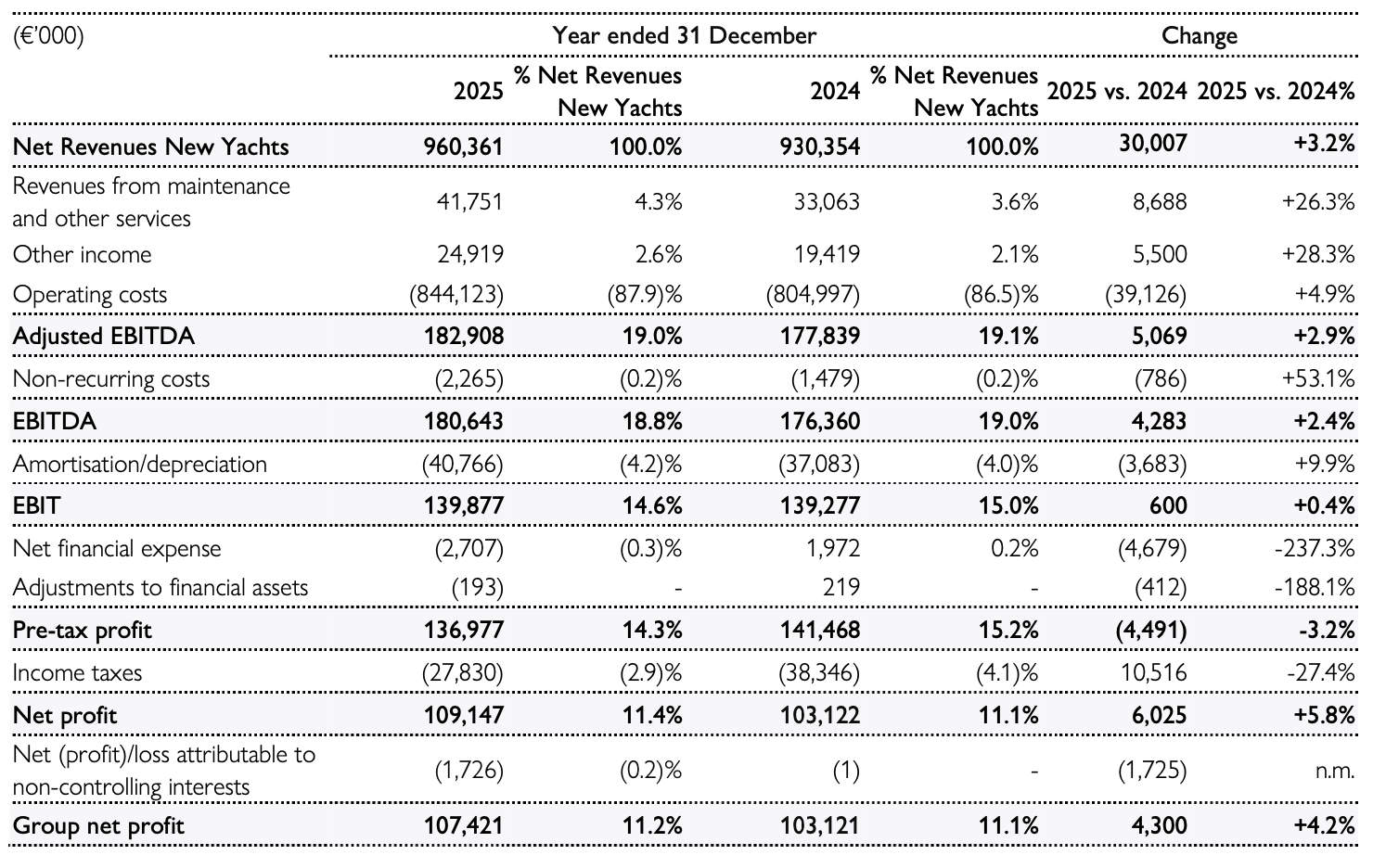

Net Revenues New Yachts1 for the year ended 31 December 2025 amounted to €960.4 million, up 3.2% compared to €930.4 million in 2024.

NET REVENUES NEW YACHTS BY DIVISION

NET REVENUES NEW YACHTS BY GEOGRAPHICAL AREA

CONSOLIDATED OPERATING AND NET RESULTS

L’EBITDA² amounted to €180.6 million, up 2.4% compared to €176.4 million in 2024. The margin on Net Revenues New Yachts is equal to 18.8%, decreasing by 20 basis points compared to the previous year, yet confirming the solidity of the Group’s business model and its ability to successfully sell and execute high-value projects. EBITDA margin thus remains broadly stable even after the full-year consolidation of Nautor Swan, whose profitability is currently below the Group average. Excluding this effect, the steady increase in operating profitability is mainly linked to the progressive and reasoned increase in average sales prices, which are mostly linked to the change in product mix in favour of larger yachts in each division, demonstrating the solidity of the business model and the Group’s ability to continue selling and executing successful projects.

EBIT amounted to €139.9 million, up 0.4% compared to €139.3 million in 2024. The margin on Net Revenues New Yachts is equal to 14.6% (compared to 15.0% in 2024), discounting the higher D&A incidence of Nautor Swan given legacy investments carried out before the acquisition.

Group Net Profit reached €107.4 million, up 4.2% compared to €103.1 million in 2024, with a double-digit margin on Net Revenues New Yachts equal to 11.2%, supported by tax benefits compensating the adverse year- on-year trend of financial income/expenses given the cash-out for 2024 acquisitions.

CONSOLIDATED BALANCE SHEET AND FINANCIAL RESULTS

The Order Backlog³ as of 31 December 2025 amounted to €1,962.8 million, compared to €1,950.1 million as of 31 December 2024, continuing to provide a solid level of visibility, especially given that 88% of it is already sold to final clients (sell-out).

The Net Backlog (all revenues still to be booked from existing contracts) as of 31 December 2025 stands at €1,002.5 million (compared to €1,019.8 million as of 31 December 2024). €618.1 million are related to 2026, benefiting from a significant level of coverage already at the beginning of the year, and providing a consistent level of visibility into future years with €384.4 million related to 2027 and beyond.

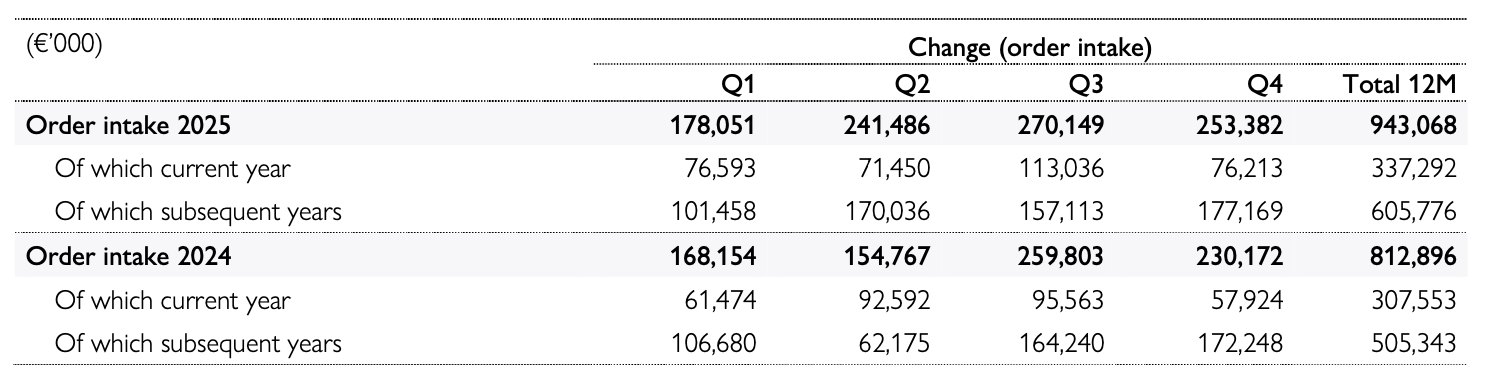

The Order Intake for the full year 2025 totalled €943.1 million, up 16.0% compared to €812.9 million in 2024, with €178.1 million in Q1, €241.5 million in Q2, €270.1 million in Q3, and €253.4 million in Q4. This result confirms the strength and positioning of the brand in the market, demonstrating solid and resilient demand across the different phases of the economic cycle.

BACKLOG

The Order Backlog³ as of 31 December 2025 amounted to €1,962.8 million, compared to €1,950.1 million as of 31 December 2024, continuing to provide a solid level of visibility, especially given that 88% of it is already sold to final clients (sell-out).

The Net Backlog (all revenues still to be booked from existing contracts) as of 31 December 2025 stands at €1,002.5 million (compared to €1,019.8 million as of 31 December 2024). €618.1 million are related to 2026, benefiting from a significant level of coverage already at the beginning of the year, and providing a consistent level of visibility into future years with €384.4 million related to 2027 and beyond.

The Order Intake for the full year 2025 totalled €943.1 million, up 16.0% compared to €812.9 million in 2024, with €178.1 million in Q1, €241.5 million in Q2, €270.1 million in Q3, and €253.4 million in Q4. This result confirms the strength and positioning of the brand in the market, demonstrating solid and resilient demand across the different phases of the economic cycle.

BUSINESS OUTLOOK

The Sanlorenzo Group closes FY 2025 with Net Revenues New Yachts up 3.2% to €960.4 million and Group Net Profit of €107.4 million (+4.2% YoY), above expectations. The achievement of all financial targets in terms of the Guidance previously communicated to the financial markets is therefore confirmed.

Particularly noteworthy is the marked acceleration in demand across the entire portfolio: FY 2025 Order Intake amounts to €943.1 million (+16.0% YoY), €130 million higher than the previous year – supported by the success of the new models presented, the enduring desirability of the brand and the strengthening of distribution in MED, APAC and the USA. As a result, the order book remains robust, with a Gross Backlog of €1.96 billion, and of high quality, as 88% of orders is already sold to final clients, confirming both the high quality and the scarcity-driven model based on limited volumes. Net Backlog – i.e., all future revenues already contracted and yet to be recognized – stands at a level just above one billion euro, consistent with the Group’s growth profile while at the same time providing a significant level of visibility on future planning and performance.

Performance is supported by the vigorous growth of the Americas, which accelerate decisively (+35.5%), returning to a revenue mix contribution above 20%. This performance derives from a broadly significant recovery in order collection over the last 12 months, as well as deeper penetration in selected Central and South American markets, where the Group has established a local presence through new Brand Representatives, whereas these markets had previously been served from abroad. Although, starting from the second quarter of the year, the US market shows increasing uncertainty linked to the policies of the current administration – particularly with reference to trade tariffs – which temporarily interfere with purchasing propensity, the Americas remain a market of primary importance for the Group’s growth, considering the large UHNWI population, the well-rooted culture of yachting and individual wellbeing, and Sanlorenzo’s penetration in the market still below its potential. From July onwards, uncertainty related to trade tariffs decreases, and the first positive signals from US clients already materialise at the main European boat shows in September. The important Fort Lauderdale boat show, held from 29 October to 2 November, records fewer attendees than the previous year, but of much higher quality in terms of client sophistication and willingness to purchase. The event also sees the inauguration of Sanlorenzo’s new Americas headquarters at the iconic Pier Sixty-Six luxury complex, a key milestone for the expansion of our brand and customer experience in the United States. Conversely, Latin America shows strong momentum, more than compensating in the second and third quarters for the cautious approach of US clients.

Also particularly significant is the performance of the APAC area (+5.1% in Net Revenues New Yachts), where the Sanlorenzo Group continues to grow and gain market share. The owned sales and service network – Simpson Marine – has been fully integrated and is proving to be an important competitive advantage in meeting the needs of an increasingly sophisticated clientele, both in the sales phase and in after-sales. APAC delivers a progressively increasing contribution in terms of Order Intake, quarter after quarter, and confirms itself as a highly strategic market for the Group given the gradual expansion of infrastructure and the strengthening of yachting culture, underpinning higher future penetration among the UHNWI population, still significantly lower than in Europe and the Americas. Through the Simpson Marine platform, with extensive

coverage and a local-for-local approach, the Sanlorenzo Group continues to pursue a regional expansion strategy aimed at entering new markets such as Australia and Japan, as well as strengthening its presence in strategic markets such as Thailand. Europe records slight growth (+1.3%), confirming the robustness of the Group’s historical markets and the deep loyalty of the “Sanlorenzo Customer Club of Connoisseurs”, a source of repeat purchases over time in line with the launch cycles of new models featuring ever more innovative content both in terms of concept design and onboard technology, as well as dimensional upgrades. The Cannes, Genoa and Monaco boat shows in September strongly confirm these dynamics, resulting in growing order collection also in Q3, strongly supported by the success of the new models presented – SL110A, SX120 and SD132 – which further fuel the upselling dynamics over time among recurring clients.

In MEA, Net Revenues New Yachts decline by 28.0%, reflecting a challenging comparison base versus the exceptional performance of 2024 and the natural volatility typical of a low-volume, high-ticket market. Despite this temporary effect, the area maintains growing relevance in the global yachting landscape, supported by strong wealth creation, a high concentration of UHNWIs and the expansion of infrastructure supporting ultra-high-end experiential luxury. Management, considering the events that have occurred in the days immediately preceding the date of this document, is closely monitoring developments and the potential impact of the situation in the Middle East following the outbreak of the conflict with Iran. Excluding African countries, which in 2025 account for approximately 1.4% of Net Revenues New Yachts, the Middle East area represented 7.7% of Net Revenues New Yachts in 2025. On the other hand, the resulting strengthening of the USD against the Euro is a positive factor for the US market.

On the strategic front, the integration of the Nautor Swan Group continues successfully, benefiting from significant synergies in procurement, the sharing of manufacturing know-how, savings in structural fixed costs and the strengthening of the commercial footprint. Product development progresses rapidly, with the newly presented Swan Alloy line – aluminium sailing superyachts from 44 to 65 metres – expected to provide a boost to growth, alongside new partnerships such as the agreement signed in March with Edmiston for brokerage in the United States. In parallel, the APAC distribution network, led by Simpson Marine, successfully completes its integration phase and now represents a solid strategic platform to capture the region’s significant long-term growth potential. In addition to the new Swan Alloy line, the Group is developing a further new line – Swan Scape – to broaden the offering to the so-called bluewater market segment, for clients who prioritise comfort and greater internal volume over performance.

Sustainable innovation, a cornerstone of the “Road to 2030” strategy, continues to represent a distinctive element and a competitive advantage for the Group. The path towards carbon neutrality progresses consistently, as demonstrated by the strategic partnership with MAN for the construction of the first 50X-Space superyacht featuring bi-fuel propulsion powered by green methanol, with launch expected in 2030. This project, together with the development of new hybrid and hydrogen solutions and the awards received by Nautor Swan for its advanced propulsion systems, confirms Sanlorenzo’s pioneering role in the green transformation of global yachting.

More broadly, the Group continues to benefit from the competitive advantage derived from its differentiated business model: high-end positioning, the uniqueness of a made-to-measure product, and a strong link with the world of design and innovation. The union of the Sanlorenzo and Nautor Swan brands – each with its own exclusive and non-overlapping identity – consolidates the creation of a unique yachting hub: the very best of motor and sailing yachting. These foundational elements underpin the Group’s ability to sustain and accelerate over the long term its virtuous growth trajectory, reinforcing confidence in future potential.

In a market affected in the short term by unpredictable external factors – such as continuous shifts in the scenario regarding United States trade policies as well as the military conflict in the Middle East – Sanlorenzo continues to stand out for positioning, innovation and scarcity of volumes, anticipating the needs of future owners, who are increasingly oriented towards wellbeing, longevity and the quality of their leisure time, which is typically scarce.

2025 CONSOLIDATED SUSTAINABILITY REPORT

The Board of Directors has reviewed and approved the 2025 Consolidated Sustainability Report, marking the second reporting exercise in compliance with Italian Legislative Decree no. 125 of 6 September 2024, issued in implementation of Directive 2022/2464/EU (Corporate Sustainability Reporting Directive) and the requirements of EU Regulation 2020/852 of the European Parliament and Council, along with related delegated regulations.

The Consolidated Sustainability Report has been prepared in accordance with the European Sustainability Reporting Standards (ESRS) issued by the European Commission and includes information on the Sanlorenzo Group’s activities related to environmental, social, and governance (ESG) matters.

The Group pursues a balanced approach between financial, environmental, and social objectives, monitoring and reporting its commitment within this document through a comprehensive and responsible 360-degree approach. This includes a strong focus on the sustainability of products and processes, human resources and the supply chain.

PROPOSAL FOR THE ALLOCATION OF PROFIT

In accordance with the dividend policy approved on 9 November 2019, the Board of Directors has resolved to propose to the Shareholders’ Meeting the distribution of a dividend of €1.05 per share for the 2025 financial year, representing a payout ratio of 34.6% of consolidated Group net profit and a YoY increase in line with net income growth. Parent company Sanlorenzo S.p.A. Net Profit at €90.4 million.

If approved by the Shareholders’ Meeting, the dividend will be paid on 20 May 2026, with the ex-dividend date set for 18 May 2026 and the record date on 19 May 2026.

OTHER RESOLUTIONS

The Board of Directors has approved the Report on corporate governance and ownership structures pursuant to Article 123-bis of Italian Legislative Decree no. 58 of 24 February 1998, as well as the Report on the policy regarding remuneration and fees paid pursuant to Article 123-ter of the same decree.

The Board of Directors has also favorably acknowledged the report of the Lead Independent Director and has confirmed the independence status of the Directors Licia Mattioli, Leonardo Luca Etro, Francesca Culasso and Marco Francesco Mazzù, both pursuant to Italian Legislative Decree no. 58 of 24 February 1998 and Recommendation 7 of the Corporate Governance Code, also in light of the quantitative and qualitative criteria for assessing significance as confirmed and resolved by the Board of Directors on 14 March 2023⁴. A similar positive verification was also carried out with respect to the members of the Board of Statutory Auditors.

NOTICE OF CALL OF THE ORDINARY SHAREHOLDERS’ MEETING

The Board of Directors has conferred powers on the Chairman and Chief Executive Officer to convene the Ordinary Shareholders’ Meeting on 24 April 2026, on first call, in accordance with the law.

The Board of Directors resolved to submit to the Shareholders in ordinary session:

– the approval of the separate financial statements as of 31 December 2025 and the proposal for profit allocation;

– the Report on the policy regarding remuneration and remuneration paid, pursuant to Article 123-ter of Italian Legislative Decree no. 58 of 24 February 1998;

– the adoption of the “2026 Performance Shares Plan” and the “Second Simpson Marine Plan”;

– the authorization to purchase and dispose of treasury shares.

The notice of the Shareholders’ Meeting and all related documents will be made available to the public, in accordance with current provisions, at the Company’s registered office in Via Armezzone 3, Ameglia (SP), in the “Corporate Governance/Shareholders’ Meeting” section of the Company’s website (www.sanlorenzoyacht.com) and on the eMarket Storage mechanism (www.emarketstorage.it).

SANLORENZO GROUP

RECLASSIFIED INCOME STATEMENT AS OF 31 DECEMBER 2025

SANLORENZO GROUP

RECLASSIFIED STATEMENT OF FINANCIAL POSITION AS OF 31 DECEMBER 2025

SANLORENZO GROUP

NET FINANCIAL POSITION AS OF 31 DECEMBER 2025

SANLORENZO GROUP

RECLASSIFIED CONSOLIDATED STATEMENT OF CASH FLOWS AS OF 31 DECEMBER 2025

1 Net Revenues New Yachts are calculated as the algebraic sum of revenues from contracts with customers relating to the sale of new yachts (recognised over time with the “cost-to-cost” method) and pre-owned yachts, net of commissions and trade-in costs of pre- owned boats.

2 EBITDA is calculated by adding amortisation/depreciation expenses to operating profit/loss.

3 Order backlog is calculated as the sum of the value of all orders and sales contracts signed with customers or brand representatives relating to yachts for delivery or delivered in the current financial year or for delivery in subsequent financial years. For each year, the value of the orders and contracts included in backlog refers to the relative share of the residual value from 1 January of the financial year in question until the delivery date. Backlog relating to yachts delivered during the financial year is conventionally cleared on 31 December.

4 These are the criteria originally established by the Board of Directors on 16 March 2021 and confirmed by the Board of Directors on 14 March 2023, as outlined in the Report on corporate governance and ownership structures for the 2024 financial.

Opening image: the Sanlorenzo SX120

(Sanlorenzo Spa: actual results confirm 2025 guidance met at all levels – Barchemagazine.com – March 2026)